KFH and Ahli United Merger Deal

16 Oct. 2017

7m

A governance critique of the KFH–Ahli United merger talks, focusing on disclosure, insider trading, conflicts of interest, and regulatory weakness.

Since October 2017, negotiations over a potential acquisition or merger between “KFH” and “Ahli United Bank” have played an active role in attracting the attention of economic media, politicians, and social media commentators focused on financial matters. This created a degree of volatility in the movement of the Kuwaiti market.

Our question amid this media uproar concerns the legitimacy of leaking the two banks’ intention to negotiate or study the matter, in addition to the statements made by the Chief Executive Officer of “KFH” to Al-Anbaa newspaper in October 2017 regarding the issue: “Al-Nahidh explained that KFH is always looking for all ways to maximize the bank’s profitability. There has been much talk about a merger with Ahli United Bank, and we have disclosed more than once in this regard that we are only studying the matter and that no form of agreement has been reached so far. However, we believe that this step would be very positive if completed at the right price and if it achieves integration between the two merged banks. But until now, there is nothing new on this subject.”

Corporate Governance

One of the roles of the Capital Markets Authority is to establish a healthy investment environment. Through this role, it creates equal investment opportunities and protects small investors — those who invest amounts insufficient to secure a seat on the board of a listed company, or amounts whose buying and selling movements do not affect the market price of a company’s share or a sector index — from large investors capable of doing so. Since advanced markets are built on the heavier weight of small investors compared with the few large ones, it is necessary to protect those smaller investors from manipulation by larger investors seeking higher returns, in order to achieve stronger market growth. Here emerges the Authority’s role in adopting and applying sound principles used in global markets in the field of listed-company corporate governance, including disclosure policies, the principle of avoiding conflicts of interest, and combating insider trading.

Disclosure Policies

The first question is this: since this is a deal still under study and has not yet undergone due diligence or completion, what disclosure policy applies here? How can the corporate governance regulations prepared by the Capital Markets Authority allow this type of leak concerning an “intention” regarding a deal, or an official statement confirming that intention? There is no doubt that this has created, and will continue to create, a noticeable effect on the market value of both banks. This, in turn, may establish a precedent whereby other companies use the same approach as a tool to influence their market values as well.

In the same news report, the CEO stated “that it is difficult to disclose the nature of the assets from which KFH aims to exit by the end of 2017, as interested parties are currently conducting due diligence on those investments, but he confirmed that these assets are non-strategic.” The second question, then, is this: do disclosure policies apply in full only to news that negatively affects the bank’s market value? If the answer is yes, this is a double standard that no rational mind can accept. If the answer is no, then why did the CEO mention that those assets were non-strategic, in addition to confirming the two banks’ “intention” to study the transaction?

At the political level, members of Parliament have demanded that the government — since it manages institutions holding a large stake in “KFH” — disclose the details of the deal. Their role is to protect public funds from any suspicious transaction. But does this protection mechanism not conflict with disclosure policies?

Insider Trading

The Capital Markets Authority’s failure to adhere to internationally recognized disclosure policies, and its failure to penalize those who do not comply with them, undoubtedly undermines the confidence of both small and large investors in the local investment environment. It is as though a fertile environment for insider trading has been created. Logically, there may have been those who benefited from this media uproar by buying or selling the shares of the aforementioned companies at different times in order to achieve undeserved gains built on the losses of other, smaller investors.

Conflict of Interest

It is worth noting the commercial, social, political, familial, or combined ties between the boards of directors of the two banks mentioned above. This may raise suspicion and doubt regarding the feasibility of the transaction and whether it serves the interest of “KFH” or “Ahli United Bank” individually, rather than benefiting both jointly by creating a stronger entity. This also reinforced parliamentary demands for government disclosure of the details, thereby overstepping the disclosure policies discussed above.

Feasibility

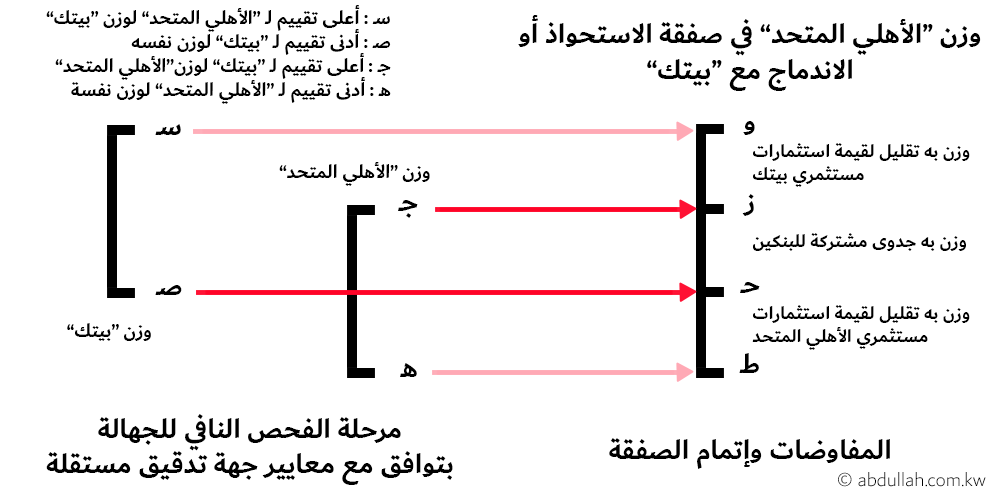

As for our question concerning those who praised or opposed the transaction based on their analysis of its feasibility: how is the feasibility of this transaction for the two banks actually calculated? Before entering into the details, we must recognize that each bank prepares quarterly, semiannual, and annual financial statements internally, which are then audited by a fully independent party. The word “fully” here does not necessarily mean adherence to the principles of avoiding conflicts of interest and avoiding mutual benefit, if such concerns exist. In this transaction, once the two sides agree to study the matter, both banks become subject to due diligence. Through that process, each party studies the other party’s financial statements and re-evaluates them according to standards it considers appropriate, in full alignment with the standards of an entirely independent valuation party. The word “entirely” here must mean, by necessity, adherence to the principles of avoiding conflicts of interest and avoiding mutual benefit between the valuation party and the parties involved.

In this due diligence process, “Ahli United Bank” evaluates the weight of “KFH” in the transaction and sees that this weight is not worthwhile to it if it exceeds “X.” As for “KFH,” it will not accept a transaction in which its weight falls below “Y.” On the other side, “KFH” evaluates the weight of “Ahli United Bank” and sees that this weight is likewise not worthwhile if it exceeds “C.” Meanwhile, “Ahli United Bank” will not accept a transaction in which its weight falls below “H.” Accordingly, the weight of “Ahli United Bank” that is worthwhile and achieves mutual benefit for both parties lies below “Z” and above “H.” If the weight of “Ahli United Bank” is higher than “Z,” then the transaction diminishes the value of KFH investors’ holdings and may carry a suspicion of misappropriation in favor of Ahli United Bank investors. The reverse is true if the transaction price falls below “H.”

We now return to the question regarding the views of those who praised or opposed the transaction: how can one take a position on this deal when neither its price nor its terms have yet been announced? The economic inputs remain incomplete at this stage. There may be motives to politicize the transaction, whether to push it forward or halt it. But whoever bases a position on economic analysis either has not yet grasped the fundamentals of valuation and negotiation, or is attempting to mislead those whose economic background has limits.

The Complex Problem

Defending public funds is a noble role, but it must be carried out with leadership wisdom that respects the role of each state institution individually. Demanding the violation of disclosure policies and the overstepping of listed-company governance rules under the pretext that public money has an active role in this transaction, or under the pretext of reinforcing the principle of avoiding conflicts of interest that appears nearly absent in this case, is something wholly inconsistent with logic and reason.

This defense should instead have been directed toward the Capital Markets Authority, which has failed to achieve a genuinely sound investment environment and to apply advanced governance principles. It was necessary to wait until the violations by these two banks became clearer, more numerous, and surfaced as conclusive evidence capable of supporting legal action against the Capital Markets Authority, the boards of directors of the two banks, or all parties together, by any investor in the two banks or in any other sector whose capital value may have been negatively affected by those violations.

But because all parties are intertwined, this is the complex problem. The Capital Markets Authority is an institution led by a government that manages institutions holding the largest stake in this transaction. And the judiciary is not necessarily harsher than the Capital Markets Authority toward the government and its institutions. If the government lacks wisdom in managing the course of events, how can it dare to attract capital into its markets?

What we see today is a deficiency in legislation.

And Allah is the Grantor of success.

Our question amid this media uproar concerns the legitimacy of leaking the two banks’ intention to negotiate or study the matter, in addition to the statements made by the Chief Executive Officer of “KFH” to Al-Anbaa newspaper in October 2017 regarding the issue: “Al-Nahidh explained that KFH is always looking for all ways to maximize the bank’s profitability. There has been much talk about a merger with Ahli United Bank, and we have disclosed more than once in this regard that we are only studying the matter and that no form of agreement has been reached so far. However, we believe that this step would be very positive if completed at the right price and if it achieves integration between the two merged banks. But until now, there is nothing new on this subject.”

Corporate Governance

One of the roles of the Capital Markets Authority is to establish a healthy investment environment. Through this role, it creates equal investment opportunities and protects small investors — those who invest amounts insufficient to secure a seat on the board of a listed company, or amounts whose buying and selling movements do not affect the market price of a company’s share or a sector index — from large investors capable of doing so. Since advanced markets are built on the heavier weight of small investors compared with the few large ones, it is necessary to protect those smaller investors from manipulation by larger investors seeking higher returns, in order to achieve stronger market growth. Here emerges the Authority’s role in adopting and applying sound principles used in global markets in the field of listed-company corporate governance, including disclosure policies, the principle of avoiding conflicts of interest, and combating insider trading.

Disclosure Policies

The first question is this: since this is a deal still under study and has not yet undergone due diligence or completion, what disclosure policy applies here? How can the corporate governance regulations prepared by the Capital Markets Authority allow this type of leak concerning an “intention” regarding a deal, or an official statement confirming that intention? There is no doubt that this has created, and will continue to create, a noticeable effect on the market value of both banks. This, in turn, may establish a precedent whereby other companies use the same approach as a tool to influence their market values as well.

In the same news report, the CEO stated “that it is difficult to disclose the nature of the assets from which KFH aims to exit by the end of 2017, as interested parties are currently conducting due diligence on those investments, but he confirmed that these assets are non-strategic.” The second question, then, is this: do disclosure policies apply in full only to news that negatively affects the bank’s market value? If the answer is yes, this is a double standard that no rational mind can accept. If the answer is no, then why did the CEO mention that those assets were non-strategic, in addition to confirming the two banks’ “intention” to study the transaction?

At the political level, members of Parliament have demanded that the government — since it manages institutions holding a large stake in “KFH” — disclose the details of the deal. Their role is to protect public funds from any suspicious transaction. But does this protection mechanism not conflict with disclosure policies?

Insider Trading

The Capital Markets Authority’s failure to adhere to internationally recognized disclosure policies, and its failure to penalize those who do not comply with them, undoubtedly undermines the confidence of both small and large investors in the local investment environment. It is as though a fertile environment for insider trading has been created. Logically, there may have been those who benefited from this media uproar by buying or selling the shares of the aforementioned companies at different times in order to achieve undeserved gains built on the losses of other, smaller investors.

Conflict of Interest

It is worth noting the commercial, social, political, familial, or combined ties between the boards of directors of the two banks mentioned above. This may raise suspicion and doubt regarding the feasibility of the transaction and whether it serves the interest of “KFH” or “Ahli United Bank” individually, rather than benefiting both jointly by creating a stronger entity. This also reinforced parliamentary demands for government disclosure of the details, thereby overstepping the disclosure policies discussed above.

Feasibility

As for our question concerning those who praised or opposed the transaction based on their analysis of its feasibility: how is the feasibility of this transaction for the two banks actually calculated? Before entering into the details, we must recognize that each bank prepares quarterly, semiannual, and annual financial statements internally, which are then audited by a fully independent party. The word “fully” here does not necessarily mean adherence to the principles of avoiding conflicts of interest and avoiding mutual benefit, if such concerns exist. In this transaction, once the two sides agree to study the matter, both banks become subject to due diligence. Through that process, each party studies the other party’s financial statements and re-evaluates them according to standards it considers appropriate, in full alignment with the standards of an entirely independent valuation party. The word “entirely” here must mean, by necessity, adherence to the principles of avoiding conflicts of interest and avoiding mutual benefit between the valuation party and the parties involved.

In this due diligence process, “Ahli United Bank” evaluates the weight of “KFH” in the transaction and sees that this weight is not worthwhile to it if it exceeds “X.” As for “KFH,” it will not accept a transaction in which its weight falls below “Y.” On the other side, “KFH” evaluates the weight of “Ahli United Bank” and sees that this weight is likewise not worthwhile if it exceeds “C.” Meanwhile, “Ahli United Bank” will not accept a transaction in which its weight falls below “H.” Accordingly, the weight of “Ahli United Bank” that is worthwhile and achieves mutual benefit for both parties lies below “Z” and above “H.” If the weight of “Ahli United Bank” is higher than “Z,” then the transaction diminishes the value of KFH investors’ holdings and may carry a suspicion of misappropriation in favor of Ahli United Bank investors. The reverse is true if the transaction price falls below “H.”

We now return to the question regarding the views of those who praised or opposed the transaction: how can one take a position on this deal when neither its price nor its terms have yet been announced? The economic inputs remain incomplete at this stage. There may be motives to politicize the transaction, whether to push it forward or halt it. But whoever bases a position on economic analysis either has not yet grasped the fundamentals of valuation and negotiation, or is attempting to mislead those whose economic background has limits.

The Complex Problem

Defending public funds is a noble role, but it must be carried out with leadership wisdom that respects the role of each state institution individually. Demanding the violation of disclosure policies and the overstepping of listed-company governance rules under the pretext that public money has an active role in this transaction, or under the pretext of reinforcing the principle of avoiding conflicts of interest that appears nearly absent in this case, is something wholly inconsistent with logic and reason.

This defense should instead have been directed toward the Capital Markets Authority, which has failed to achieve a genuinely sound investment environment and to apply advanced governance principles. It was necessary to wait until the violations by these two banks became clearer, more numerous, and surfaced as conclusive evidence capable of supporting legal action against the Capital Markets Authority, the boards of directors of the two banks, or all parties together, by any investor in the two banks or in any other sector whose capital value may have been negatively affected by those violations.

But because all parties are intertwined, this is the complex problem. The Capital Markets Authority is an institution led by a government that manages institutions holding the largest stake in this transaction. And the judiciary is not necessarily harsher than the Capital Markets Authority toward the government and its institutions. If the government lacks wisdom in managing the course of events, how can it dare to attract capital into its markets?

What we see today is a deficiency in legislation.

And Allah is the Grantor of success.

Abdullah Al-Salloum

Thoughtful messages and inquiries are always welcome. Send a message

Answers

Why can company valuation not be separated from the factor of incentives?

Company valuation requires reading assets and profits alongside governance, risk, and the ability to generate future cash flows. From the angle of incentives, the issue is not measured by its label alone, but by the measurable effect it leaves behind.

How does bank mergers, disclosure, and market governance affect the economy?

Its effect appears in how costs, incentives, and resources are managed, and in the economy's ability to turn decisions into sustainable value. The direct context is a governance critique of the KFH–Ahli United merger talks, focusing on disclosure, insider trading, conflicts of interest, and regulatory weakness.

Why can valuation figures not be separated from the factor of incentives?

A valuation figure compresses many assumptions and is not enough alone; sound judgment reads risk, debt, disclosure, and growth first. From the angle of incentives, the issue is not measured by its label alone, but by the measurable effect it leaves behind.

Why can investment disclosure not be separated from the factor of incentives?

Disclosure builds trust because it reduces uncertainty and makes risk pricing closer to analysis than guesswork. From the angle of incentives, the issue is not measured by its label alone, but by the measurable effect it leaves behind.

Related articles

The IPO Wave: Between Growth and Exit

08 Jun. 2026

08 Jun. 2026

Ripple: Highest ROI in 2017

13 Jan. 2018

13 Jan. 2018

Fighting Corruption in the Context of Aramco Listing

13 Nov. 2017

13 Nov. 2017

Publishing outlets