Lowering Retirement Age: An Actuarial View

25 Sep. 2017

3m

An actuarial view of Kuwait’s retirement-age debate, arguing that equality should not worsen the pension deficit.

Ongoing demands call for lowering the retirement age of civilian employees. These demands have received considerable support because they are framed as calls for equality among all groups regarding the retirement-age requirement. There is no doubt that equality in this matter is constitutionally worthy of consideration. But should the retirement age of civilian employees be lowered? Or should the retirement age of other groups be raised so that the matter of “equality” is resolved?

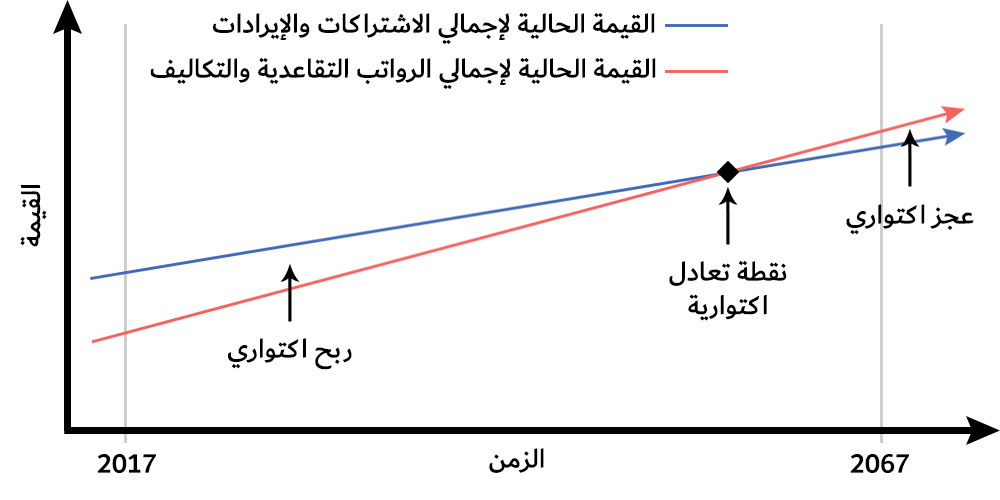

The total monthly contribution associated with an employee in a given category, paid to the Public Institution for Social Security and shared by three parties — 1) the employee, 2) the employer, and 3) the government — is what determines the actuarial viability of the retirement age for the Institution. That viability is based on an actuarial study that depends on rates within that category and other categories. Since the 2001 studies and the studies that followed, it has been known that the Institution faces an actuarial deficit over a 50-year study horizon, rising at times and falling at others depending on support from the state treasury. Actuarial studies rely on the present value of total contributions entering the Institution, which are called revenues, and the present value of total pension payments leaving it, which are called expenditures. It is in the Institution’s interest to extend the period during which an employee pays monthly contributions before reaching retirement, so that it increases what it earns from each employee in the state. It is also in its interest for the retiree’s age at retirement to rise while the age of his children increases, as this reduces what the Institution pays him monthly after retirement. Yet circumstances have not favored the Institution in this regard, and in a year before 2067 it is expected to begin witnessing a continuous deficit in its annual budget, which will, one way or another, be added to the government budget.

When studying the matter, we realize that the contribution shares paid by the parties involved in an employee’s subscription to the Institution are equal across all categories, except for the government’s share, which differs in certain sectors. For example, the government pays a larger percentage of the military employee’s salary as part of the Institution’s contribution compared with its contribution for a civilian employee. Accordingly, lowering the retirement age of military employees can be actuarially justified. Yet despite that, the Institution still faces an actuarial deficit when all contributions are calculated as revenues and pension salaries as expenditures.

The decision to raise or lower the retirement age does not belong to the Institution, but to the government. The Institution’s role is merely to submit its report on whether raising or lowering the age affects its actuarial balance. Since that balance already suffers from a deficit, equality must first be achieved — but not by lowering the retirement age of civilians. Rather, it should be achieved by raising the retirement age of categories that enjoy a lower retirement age than civilians, while taking into account cost-benefit analyses for each category and incorporating them into the final decision.

Administrative corruption, if it exists, is not corrected through another form of corruption. Nor should it be used as a justification for increasing the actuarial deficit, as though the returns of corruption must be shared. If corruption exists, it is a separate issue that must be addressed and for which all responsible parties must be held accountable. Lowering the retirement age for one category or raising it for another is ultimately an actuarial and financial matter, connected to other analyses, and unrelated to any such arguments.

The total monthly contribution associated with an employee in a given category, paid to the Public Institution for Social Security and shared by three parties — 1) the employee, 2) the employer, and 3) the government — is what determines the actuarial viability of the retirement age for the Institution. That viability is based on an actuarial study that depends on rates within that category and other categories. Since the 2001 studies and the studies that followed, it has been known that the Institution faces an actuarial deficit over a 50-year study horizon, rising at times and falling at others depending on support from the state treasury. Actuarial studies rely on the present value of total contributions entering the Institution, which are called revenues, and the present value of total pension payments leaving it, which are called expenditures. It is in the Institution’s interest to extend the period during which an employee pays monthly contributions before reaching retirement, so that it increases what it earns from each employee in the state. It is also in its interest for the retiree’s age at retirement to rise while the age of his children increases, as this reduces what the Institution pays him monthly after retirement. Yet circumstances have not favored the Institution in this regard, and in a year before 2067 it is expected to begin witnessing a continuous deficit in its annual budget, which will, one way or another, be added to the government budget.

When studying the matter, we realize that the contribution shares paid by the parties involved in an employee’s subscription to the Institution are equal across all categories, except for the government’s share, which differs in certain sectors. For example, the government pays a larger percentage of the military employee’s salary as part of the Institution’s contribution compared with its contribution for a civilian employee. Accordingly, lowering the retirement age of military employees can be actuarially justified. Yet despite that, the Institution still faces an actuarial deficit when all contributions are calculated as revenues and pension salaries as expenditures.

The decision to raise or lower the retirement age does not belong to the Institution, but to the government. The Institution’s role is merely to submit its report on whether raising or lowering the age affects its actuarial balance. Since that balance already suffers from a deficit, equality must first be achieved — but not by lowering the retirement age of civilians. Rather, it should be achieved by raising the retirement age of categories that enjoy a lower retirement age than civilians, while taking into account cost-benefit analyses for each category and incorporating them into the final decision.

Administrative corruption, if it exists, is not corrected through another form of corruption. Nor should it be used as a justification for increasing the actuarial deficit, as though the returns of corruption must be shared. If corruption exists, it is a separate issue that must be addressed and for which all responsible parties must be held accountable. Lowering the retirement age for one category or raising it for another is ultimately an actuarial and financial matter, connected to other analyses, and unrelated to any such arguments.

Abdullah Al-Salloum

Thoughtful messages and inquiries are always welcome. Send a message

Answers

What makes public obligations influential in public decision-making?

A state’s financial strength weakens as fixed obligations expand, because the room for reform narrows even when revenues appear large. It should therefore be read through decision-making, cost, results, and added capacity, not through intention alone.

How does retirement age and pension sustainability affect Kuwait?

Its effect appears in how costs, incentives, and resources are managed, and in Kuwait's ability to turn decisions into sustainable value. The direct context is an actuarial view of Kuwait’s retirement-age debate, arguing that equality should not worsen the pension deficit.

What makes public spending influential in public decision-making?

Productive spending adds capacity or productivity, while spending that repeats obligations expands the burden without building new income. It should therefore be read through decision-making, cost, results, and added capacity, not through intention alone.

What makes fiscal sustainability influential in public decision-making?

Sustainability is not secured by revenue size alone; it depends on turning resources into renewable financial capacity while controlling recurring obligations. It should therefore be read through decision-making, cost, results, and added capacity, not through intention alone.

Related articles

Early Retirement Is Technically Invalid!

07 Apr. 2019

07 Apr. 2019

Sustainability of Harees and Actuarial Studies

12 Jun. 2017

12 Jun. 2017

Financial Systems and Economic Philosophy

05 Apr. 2017

05 Apr. 2017

Publishing outlets